Why Options Chain Data Is Every Indian Trader’s Secret Weapon

The most informed traders in India’s equity markets are not simply tracking price movements — they are reading layers of data that reveal where institutional money is positioned, where the market is likely to find resistance, and how much fear or confidence exists among professional participants at any given moment. The morning routine for these traders typically begins with a check of SGX Nifty Futures to assess pre-market directional bias, followed by a deep dive into the NSE Option Chain, where the real intelligence about market structure, hedging activity, and probable price ranges is hidden in plain sight. Together, these two data sources offer a richer and more actionable picture of market conditions than price charts alone can ever provide.

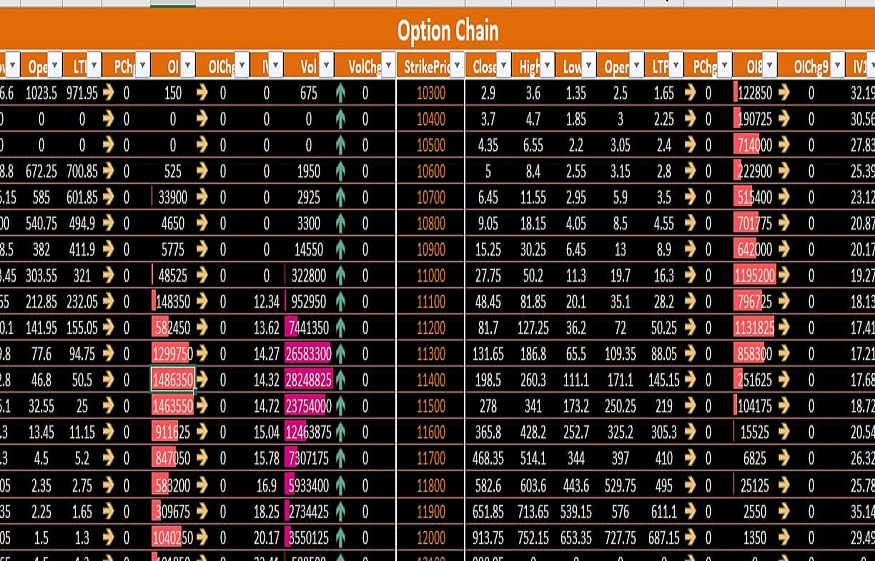

Understanding Open Interest and Why It Matters

The open interest is a very wide range of super option contracts that have not been eliminated. Unmarried is the most crucial pillar within the alternative chain, but remains widely misunderstood among retail promoters of India’s derivatives market.

Read More : How Nally Megabin Solutions from Reflex Equip Improve Storage Efficiency

When open interest usually forms at a particular call strike rate, it indicates that a large number of investors have bought calls at that level – in effect, this focus on writing calls means the index does not rise above it at the end of the period, creating what is commonly known as a wall of resistance. The index often struggles with hurdles at levels where call open interest is highest, as sellers of those options actively hedge their positions in a way that stifles the upside.

The same logic applies in reverse to established alternatives. Writing heavily on the chosen strike price indicates that investors assume the index will move above that level, developing a support floor. Each call and put has a strike fee at the highest blended free interest — called the maximum pain point — which is where the index has historically gravitated as an outdated approach, making it a valuable contextual factor for weekly options investors.

The Put-Call Ratio as a Sentiment Gauge

The placed-call ratio is one of the most followed sentiment indicators for buying and selling Indian derivatives. It is calculated by using the total free interest of the time options and dividing the total free interest of the outstanding options. A ratio above one indicates that more puts are first-rate than calls, which indicates broadly cautious or bearish market sentiment. A ratio below one indicates more appealing interests and more positive emotions.

What makes the put-to-call ratio particularly profitable is its opposite quality. Very low readings — indicating excessive optimism and heavy name buying — have traditionally preceded short-term market corrections, as excessive bullishness leaves the market at risk of pulling back as sentiment changes. Conversely, very excessive readings — reflecting excessive concern over establishment competition and the boshom — the market, just before the recovery began

Experienced traders in India use the established name ratio not as an independent marker but as a contextual setting tool that allows them to examine whether contemporary market sentiment is complacent, fearful or balanced.

Implied Volatility and What It Tells You About Market Expectations

Every option contract is priced using several variables, and implied volatility is among the most revealing. It represents the market’s collective expectation of how much the index is likely to move over the life of the option. When implied volatility is elevated, options are expensive — a reflection of uncertainty and risk aversion among market participants. When it is low, options are cheaper, signalling a calm, range-bound market environment.

For Indian traders, tracking implied volatility levels around key events — Reserve Bank of India policy announcements, quarterly earnings seasons, Union Budget presentations, and state election results — provides a powerful edge. Rising implied volatility ahead of these events signals that the market is pricing in significant uncertainty and that a sharp directional move is anticipated. Falling implied volatility post-event typically reflects relief as uncertainty resolves, and it is often accompanied by a rapid decline in options premiums even when the index direction is correct.

Understanding this volatility dynamic prevents a common and costly mistake: buying options just before a major event only to watch the premium collapse after the announcement, despite the price moving in the expected direction.

How Futures Positioning Completes the Derivatives Picture

Despite revealing an option chain focused on institutional hedging and speculative betting, futures placement tells a complementary story of directional belief. When futures open interest rises with rising costs, the formation of sparkling long positions — a sign of true bullish engagement when fees push up but futures open interest decreases, indicating little protection against new buying — indicates a weaker and equally much less sustainable fit.

Read More : How a CEO Coach in New York Helps Leaders Scale Faster

Combining this futures placement fact with option chain analysis gives derivatives investors in India a complete, three-dimensional view of market structure that pure price analysis cannot replicate.

Building a Derivatives-Informed Trading Framework

Reading futures and option chain data fluently is a skill that compounds in value over time. Traders who invest in developing this understanding gain the ability to assess not just where the market is going, but how strongly the conviction behind that move is supported by institutional positioning.

In India’s rapidly maturing derivatives market — now among the most actively traded in the world — this edge is available to any investor willing to study the data carefully, apply it with discipline, and resist the temptation to overcomplicate a process that rewards clarity and patience above all else.